Navigating through the Coronavirus Outbreak with CFDs

“A stock market decline is as routine as a January blizzard in Colorado. If you’re prepared, it can’t hurt you. A decline is a great opportunity to pick up the bargains left behind by investors who are fleeing the storm in panic”

Peter Lynch

The World Health Organization (WHO) has declared a global health emergency over the coronavirus. As at 10 Feb 2020, Covid-19 has killed more than 900 people in China and infected thousands worldwide.1 Covid-19 has sent shockwaves through the financial markets. Hong Kong and Singapore, whose economies are highly dependent on trade and global fund flows, are bound to see their economies impacted negatively.

No one can predict when this outbreak will end or the magnitude that financial markets will be impacted. What we can do, however, is focus on the things we can control.

For example:

- Investigate the market’s past behaviour during similar outbreaks of infectious diseases to anticipate magnitude of impact.

- Understand which sectors will be impacted during an infectious disease outbreak.

- Hedge our portfolio against black swan events and uncertainties.

In this article, we will be looking back in time to analyse how financial markets reacted to similar outbreaks of infectious diseases. Secondly, we will be investigating which sectors and asset classes will be impacted during an infectious disease outbreak. Last but not least, we will be looking at how Contracts for Differences (CFDs) can be used for hedging in times of such uncertainties!

Infectious Epidemics and Past Market Performance

“History doesn’t repeat itself, but it often rhymes”

Mark Twain

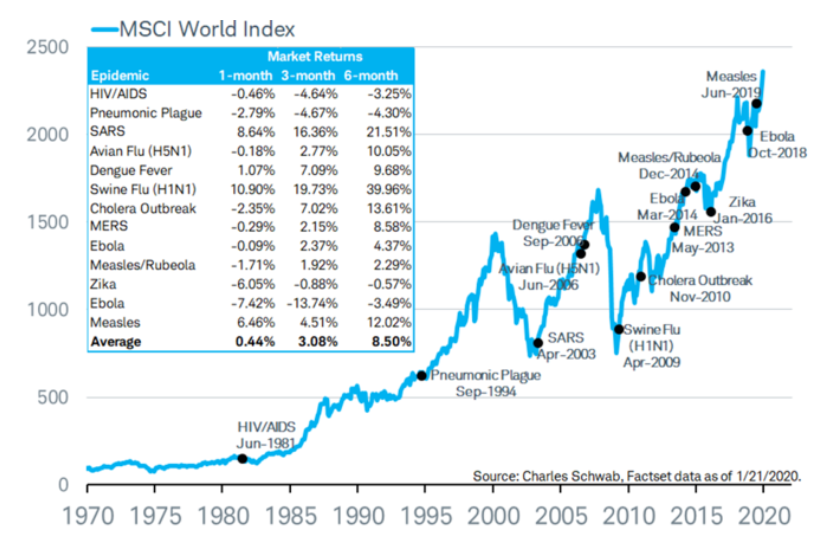

When attempting to analyse and investigate a particular event, it is ideal to look back into history to find out how markets reacted during that period in time. The good news is that historical data does tell us that financial markets have been relatively resilient to past infectious epidemics. The MSCI World Index is a collection of 1655 counters from developed countries, including Japan, Hong Kong and Singapore. From the MSCI World Index chart below, we can conclude that the global economy was relatively resilient to infectious epidemics. Approximately three months after the SARS epidemic, the MSCI return 16.36%.2

MCSI World Index2

In our opinion, the closest parallel to the coronabirus was the SARS epidemic. According to data gathered from WHO and the Centres for Disease Control and Prevention, the SARS epidemic resulted in 8100 infected and 774 deaths. The fatality rate of SARS amounted to 9.5%.3 The fatality rate of Covid-19 ranges around 2%4 (subjected to change) as of early February 2020.

Given the similarities between SARS and Covid-19’s outbreak, we decided to investigate the impact that the SARS epidemic had on open economies such as Hong Kong and Singapore. The first case of SARS in China was reported on Saturday 16 November 2002. Therefore, we used Monday 18 November 2002 as the start date to analyse how markets would react to the SARS epidemic.5 Similar to the MSCI World Index, an initial 3-month decline was followed by a strong uptrend a year later.

| Start Date (18/11/2002) | 3 Months Return | 6 Months Return | 9 Months Return | 12 Months Return |

| Straits Times Index | -9.53% | 6.64% | 15.13% | 24.82% |

| Hang Seng Index | -7.24% | -8.00% | 5.09% | 23.02% |

Sectors Impacted

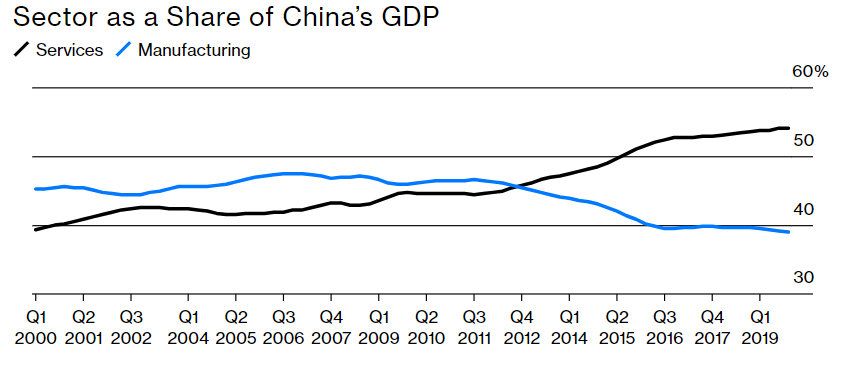

The Covid-19 Outbreak occurred near the time of Chinese New Year 2020, a rather untimely period where travelling and retail spending is generally at its peak. China’s GDP now amounts to 17% of the Global GDP as opposed to 4% in 2003. This infectious epidemic would put China GDP growth at 5.7%, and will be China’s lowest GDP growth in nearly three decades.6 During the SARS period in 2003, the Service industry amounted to 42% of China’s GDP. As of 2019, the Service industry amounted to 54% of China’s GDP. China’s GDP now amounts to 17% of the Global GDP as opposed to 4% in 2003.7

International Monetary Fund

In an event of an epidemic outbreak, industries such as tourism, and its several economic and sub sectors such as transport, hospitality, and retail spending will feel the first brunt of impact. Below is a table of the counters and their respective industries that were affected.

| Name | Exchange | Contract Code | Industry | CFD Margin Requirement | Total Return (060120 – 060220) |

| CHINA SOUTHERN AIRLINES CO-H | HKSE | 1055 | Airlines | 30% | -20.77% |

| CHINA EASTERN AIRLINES CO-H | HKSE | 0670 | Airlines | 30% | -20.18% |

| SATS LTD | SGX | SATS | Airport Services | 10% | -12.21% |

| COMFORTDELGRO CORP LTD | SGX | CFD | Transportation | 10% | -9.32% |

| FAR EAST HOSPITALITY TRUST | SGX | FEHT | Hotel & Resort REITs | 20% | -8.67% |

| MALAYSIA AIRPORTS HLDGS BHD | KLSE | MAH | Airport Services | 20% | -8.20% |

| HAIDILAO INTERNATIONAL HOLDI | HKSE | 6862 | Consumer Services | 30% | -8.00% |

| SASSEUR REAL ESTATE INVESTMENT | SGX | SASUR | Retail REITs | 20% | -7.87% |

| MTR CORP | HKSE | 0066 | Transportation | 20% | -7.54% |

| EAGLE HOSPITALITY TRUST | SGX | EGHT | Hotel & Resort REITs | 20% | -7.27% |

| SIA | SGX | SIAA | Airlines | 10% | -4.77% |

| CHINA AIRCRAFT LEASING GROUP | HKSE | 1848 | Capital Goods | 40% | -3.95% |

| LENDLEASE GLOBAL COMMERCIAL | SGX | LREIT | Retail REITs | 20% | -1.08% |

| STARHILL GLOBAL REIT | SGX | SHG | Retail | 20% | -0.51% |

| SPH REIT | SGX | SPHS | Retail REITs | 10% | 0.00% |

| CAPITALAND MALL TRUST | SGX | CTM | Retail REITs | 15% | 3.30% |

| CAPITALAND RETAIL CHINA TRUS | SGX | CRCT | Retail REITs | 20% | -4.403% |

| BHG RETAIL REIT | SGX | BHGR | Retail REITs | 20% | -5.109% |

| YTL HOSPITALITY REIT | KLSE | SRET | Hotel & Resort REITs | 30% | -5.109% |

| TRIP.COM | NASDAQ | TCOM | Travel Services | 20% | 0.09% |

| BOOKING.COM | NASDAQ | BKNG | Travel Services | 15% | -5.28% |

Data retrieved from Bloomberg, Total Returns over 1 month

During uncertainties, Gold and other precious metals are often favoured. However, not all industries will feel the brunt of the bear market. According to table below, healthcare supplies and glove manufacturing counters have seen their counters appreciate.

| Name | Exchange | Contract Code | Industry | CFD Margin Requirement | Total Return (060120 – 060220) |

| UG HEALTHCARE CORP LTD | SGX | UGHC | Health Care Supplies | 50% | 64.234% |

| QT VASCULAR LTD | SGX | QTVC | Health Care Equipment | 70% | 33.333% |

| MEDTECS INTERNATIONAL CORP | SGX | MIC | Health Care Supplies | 100% | 152.5% |

| SUPERMAX CORP BHD | KLSE | SUM | Health Care Supplies | 30% | 25.55% |

| TOP GLOVE CORP | KLSE | TOG | Health Care Supplies | 30% | 20.99% |

| RIVERSTONE HOLDINGS | SGX | RVS | Health Care Supplies | 20% | 8.60% |

| HARTALEGA HOLDINGS | KLSE | HTH | Health Care Supplies | 20% | 6.11% |

| RAFFLES MEDICAL | SGX | RAFSP | Health Care Supplies | 20% | 0.98% |

| COMFORT GLOVE | KLSE | IRC | Commodity Chemicals | 20% | 12.26% |

| HARTALEGA HOLDINGS | KLSE | HTH | Health Care Supplies | 20% | 6.11% |

Data retrieved from Bloomberg, Total Returns over 1 month

If one believes that the information factored into certain counters affected is temporary and reflects something shorter than his holding period, it may be wise to long and value cost average into these respective counters with strong balance sheets and free cash flow stability.

However, if one believes the uptrend in certain counters was due to a knee jerk reaction or that the down trend is going to continue, it may be ideal to short these counters. CFDs are popular tools used for short selling as they have no contract expiry date and can bypass the need of share borrowing. Check out our guide on CFD short selling here!

Hedge Your Portfolio against Rising Uncertainty

“The Markets generally are unpredictable, so that one has to have different scenarios. The idea that you can actually predict what’s going to happen contradicts my way of looking at the Market”

George Soros

Contrary to popular opinion, CFDs are not restricted to technical traders. Long term investors can utilise CFDs to hedge their positions against unforeseen events and uncertainties.

One can use CFDs as a hedge in these 2 possible scenarios:

1) When the price of your existing positions has already moved/is moving against you.

2) When you anticipate future gains in your existing positions to be marginal due to increasingly negative market sentiment.

A practical application for most buy and hold investors would be to use CFD indices for hedging. This is an alternative to using a CFD to short sell each individual counter which they are currently holding. The benefits of hedging using CFD indices is that CFD indices generally have minimal commission fees and low margin requirements.

CFD Trading Example

George is a long-term investor with a $100,000 portfolio of stocks. Assuming most of George’s equity holdings are main constituents of Index X.

Let us assume the following:

1 Contract value of Index X = $3300

Amount of Index X Contracts: $100,000/$3300 = 30

Given the price of Index X, George would need approximately 30 contracts to perform a partial hedge.

Assuming Index X has a margin requirement of 5%, and has an exposure of $1 per point, George’s Initial Capital outlay for Index X would have been:

$3300 * 5% * 30 = $4950 with a $99,000 short exposure.

A decline in the value of George’s equity portfolio would have been potentially offset by the gains in his short index position.

Do note that this example is just a conceptual example on hedging. Charges such as commission and financing charges are not included in this example.

This scenario is ideal for people seeking capital preservation for their nest egg as opposed to high frequency trading or speculation.

Summary

“Mr Market’s job is to provide you with prices. Your job is to decide whether it is to your advantage to act on them. You do not have to trade with him just because he constantly begs you.”

Benjamin Graham

Truth be told, no one has a crystal ball that can predict when an infectious epidemic will come, or when it will end. In my opinion, the best way to deal with such events is to learn from history and focus on what you can control. You can control your emotions and the price you pay. I sincerely hope that you have found value in this article. Till next time folks!

Begin your Trading Journey with us!

References:

[1]https://www.aljazeera.com/news/2020/01/timeline-china-coronavirus-spread-200126061554884.html

[2]https://www.schwab.com/resource-center/insights/content/will-virus-outbreak-lead-to-market-breakdown

[3]https://www.cdc.gov/sars/about/fs-sars.html

[4]https://www.worldometers.info/coronavirus/coronavirus-death-rate/

[5]https://www.cdc.gov/about/history/sars/timeline.htm

[6]https://www.straitstimes.com/business/economy/chinas-economy-will-grow-at-57-in-2020-oxford-economics-says

[6]https://www.bloomberg.com/news/articles/2020-01-31/the-coronavirus-is-more-dangerous-for-the-economy-than-sars

More Articles

Is Hong Kong Losing Its Shine?

Is Hong Kong Losing Its Shine? What is China’s grand plan for Hong Kong in the Greater Bay Area? Read more about Hong Kong’s role as an international financial hub in the heart of China.

What is FX CFD & Why Should You Trade Them?

Did you know that the forex market is open 24 hours a day, and is the world’s largest market in terms of daily transactional volume? Understand the basic fundamentals of Forex trading with us!

Short Selling with CFDs! Profit Your Position.

If you have never attempted short-selling before, maybe it is time to start as you are losing out on 50% of the opportunities in the market. Let us take a look at some reasons to short-sell!

Disclaimer

This material is provided to you for general information only and does not constitute a recommendation, an offer or solicitation to buy or sell the investment product mentioned. It does not have any regard to your specific investment objectives, financial situation or any of your particular needs. Accordingly, no warranty whatsoever is given and not liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of your acting based on this information.

Investments are subject to investment risks. The risk of loss in leveraged trading can be substantial. You may sustain losses in excess of your initial funds and may be called upon to deposit additional margin funds at short notice. If the required funds are not provided within the prescribed time, your positions may be liquidated. The resulting deficits in your account are subject to penalty charges. The value of investments denominated in foreign currencies may diminish or increase due to changes in the rates of exchange. You should also be aware of the commissions and finance costs involved in trading leveraged products. This product may not be suitable for clients whose investment objective is preservation of capital and/or whose risk tolerance is low. Clients are advised to understand the nature and risks involved in margin trading.

You may wish to obtain advice from a qualified financial adviser, pursuant to a separate engagement, before making a commitment to purchase any of the investment products mentioned herein. In the event that you choose not to obtain advice from a qualified financial adviser, you should assess and consider whether the investment product is suitable for you before proceeding to invest and we do not offer any advice in this regard unless mandated to do so by way of a separate engagement. You are advised to read the trading account Terms & Conditions and Risk Disclosure Statement (available online at www.poems.com.sg) before trading in this product.

Any CFD offered is not approved or endorsed by the issuer or originator of the underlying securities and the issuer or originator is not privy to the CFD contract. This advertisement has not been reviewed by the Monetary Authority of Singapore (MAS).